What Happened to My Discount?

With all the changes that have happened, some people think that they are no longer getting any kind of discount. The good news is that is not true. ICBC still rewards experienced and claim-free drivers with discounts on their insurance rates.

The discount system has undergone some changes. Before you had a CRS level and now you have an Individual Driver Factor. They both provide drivers with either a discount or a surcharge but they get there in different ways.

The Old CRS Discount Model

ICBC’s old model was called the Claim Rated Scale, or CRS for short. The system worked like a set of stairs. Each year claim-free, you would go down a step, earning a discount from where you were before. You could earn up to a maximum of 20 years on the scale. An at-fault accident would make you climb back up. How much you moved depended on where you started from and how many accidents you had.

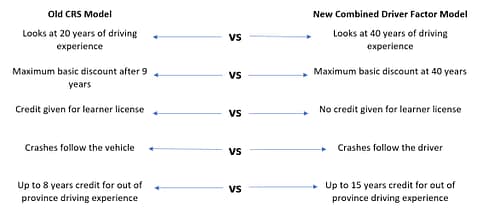

While this model was usually simple to understand, not all aspects of it were fair. New residents would not qualify for a discount in the CRS model unless they could supply a verifiable Claims History Letter. Depending on where you were coming from and your circumstances, this was sometimes difficult to obtain. In some cases, clients who had been driving many years, but hadn’t insured their own vehicle, had to start over with zero discount.

BC drivers would reach the maximum basic discount on the scale after only 9 years of driving history. This means that drivers who were accident free for 20 or more years, were still paying the same basic rate as a driver who had been accident free for 9 years.

Accident claims would not necessarily be reflected in the at-fault driver’s premiums either. It was a vehicle based system – accidents would follow the vehicle they happened in first. If that policy ever got cancelled, then it would turn up with either the vehicle owner or the at-fault driver. So if you loaned your car out and that driver crashed your vehicle, you would be stuck paying the higher premiums even though you aren’t a riskier driver.

The New Driver Factor Model

The model ICBC now uses is the Combined Driver Factor, or CDF for short. Each BC licensed driver is assigned an Individual Driver Factor. It is also based on the number of years of claim-free driving and accidents that a driver has. The number is expressed in a decimal value, such as 1.173. The lower the number, the better the discount. An at fault crash makes that number get larger.

To check your Driver Factor, head over to ICBC. Make sure you have your driver’s license on hand and an email address to send the report to.

When you insure your vehicle in the Driver Factor model, you will be asked to list all the drivers that will regularly operate your vehicle and which of them will be the principal driver. The Individual Driver factor of the principal driver will be given 75% of the weight in the overall premium. The remaining 25% will be from the listed driver who has the highest Individual Driver Factor. These two Individual Driver Factor numbers then become the Combined Driver Factor for that vehicle.

In this model, you can get credit for twice as much driving history, up to 40 years. However, this model also treats at-fault accidents more seriously. An at-fault accident will impact a driver on a decreasing basis for 10 years.

Drivers that move to BC will get credit for their out of province experience based on their driver’s abstract information. Instead of looking at just 8 years of history, ICBC will now consider up to 15 years of driving experience. Drivers only need to request a driving abstract from each the places they held a valid driver’s licence, instead of contacting each company they bought insurance from.

Another big difference in the new model is that it treats learner drivers differently. ICBC found that learner drivers were not likely to cause a crash, but novice drivers still crashed at a rate expected of an inexperienced driver. The old model awarded each year with a learner license with a discount. By the time some drivers got their novice license and start driving unsupervised, they already had the maximum discount. The new model starts counting discount years when a driver receives their novice license. Doing this means the premiums charged to novice drivers matches with their risk of causing a crash.

The driver based model also changes where premiums increase after a crash. Instead of having accidents follow the vehicle they happened in, they will now follow the driver who caused them. It changes their Individual Driver Factor, which will potentially change the premium for any vehicle for which they are a listed driver.

If you need to find out more information about your own specific situation, feel free to stop by one of our offices for more information! Remember to bring the names and birth dates of all drivers to make sure we can give you accurate information.